Some of my favorite books are science fiction. It’s always fun to imagine some fundamental change in technology and then see how at least one person thinks it might play out.

But I’m struck by a weird asymmetry in science fiction: it’s way easier to imagine dystopias than utopias. Most worlds of science fiction are markedly worse than ours in pretty catastrophic ways. Utopian science fiction barely exists.1

Some of that asymmetry may be simply that stories require conflict, and a dystopian society naturally generates conflict that makes for an interesting story. A novel where everyone’s happy and leads contented, fulfilling lives is, well, kinda boring.

Recently, I’ve been thinking the reason for this negative skew may be different: perhaps human beings just aren’t designed to view any world as utopian. We’re both problem-centered in our focus, making us ignore the things that are going well, and our drives and needs are frequently misaligned so, even when we get what we want, we don’t always get what we need.

Why are We So Rich, Yet Everyone Feels Poor?

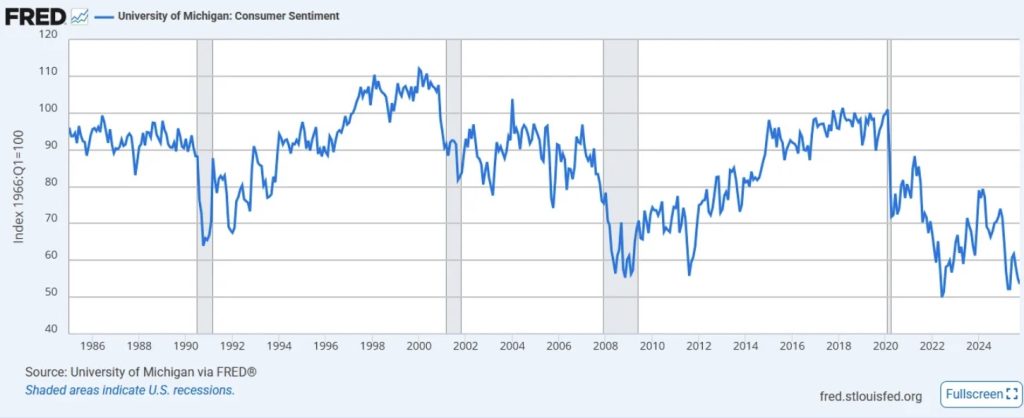

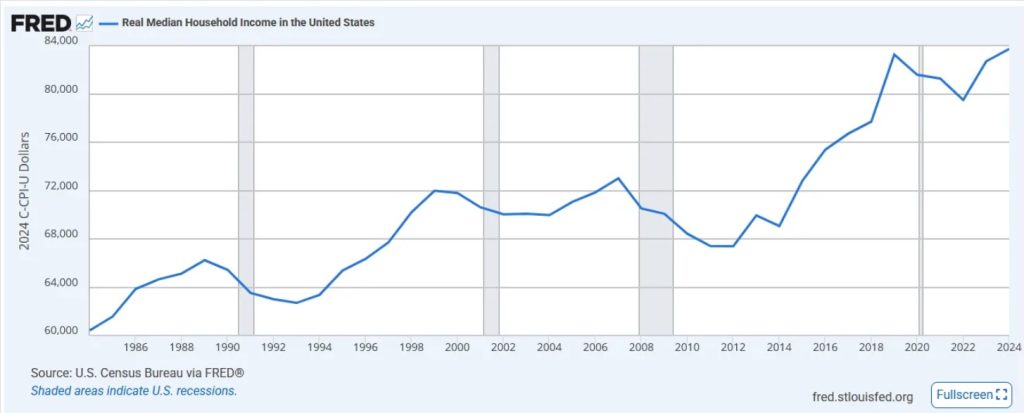

I’ve spent a lot of time thinking about Scott Alexander’s essay on the vibecession. To summarize briefly: Americans think the economy sucks. Yet, by almost all measures, it is doing fantastically well. Alexander tries to diagnose why economists and everyday people disagree to such a large extent.

The knee-jerk reaction is that the economists are just wrong. But Alexander goes to great lengths to explain why this probably isn’t true. In most ways economists can measure, people aren’t doing too badly: unemployment is down, inflation is under control, and, for Americans at least, they’re much, much richer than almost everywhere else in the world, both in terms of the very top and also for most of the middle.

I know it’s fashionable in certain circles to dismiss economists entirely as being an apologia for laissez-faire capitalism and right-wing ideologues. But I think this criticism mistakes a certain subset of economists (who are currently dwindling in number) for the field as a whole. There are plenty of left-leaning economists, and the professional incentives hardly align with suppressing pessimism about the state of the economy for everyday people.

So, it seems likely to me that if there was a really good case for why the economy is actually terrible and the vibecession were justified, economists would endorse it.

My personal guess is that pessimism about the economy can probably be explained by an overall increasing negativity in news media. When people are asked about their personal situation, they tend to respond more positively, but when asked about “the economy”, the question expands to other people, and respondents are more likely to rely on what they hear from news reports.

News has gotten a lot more negative. But that simply bumps the question up further: why is the news so pessimistic? Why does our society feel increasingly dystopian?

You Get What You Want, But You Can’t Always Get What You Need

Media pessimism is probably best explained by consumer preference. People are more likely to read about bad news.

This doesn’t mean people want bad things to be happening in the world. It’s simply that if everything is good, we don’t need to hear about it. Our evolved preference is to seek out information when there are potential threats.

This makes an asymmetry in news production that’s similar to the one we see in science fiction. Feel-good stories are the minority. When they do appear, they’re often kind of boring. Feel-bad or feel-scared stories dominate the headlines because these drive reader interest.

We have always wanted to hear bad news, but the vibecession is recent. The reason we feel particularly pessimistic about the world today is that media has become increasingly optimized to give us what we want. The hypercompetitive, algorithm-driven media environment is simply a much more desirable product, from the perspective of consumer preferences, than the more boring newspaper era.

This isn’t limited to news media pessimism. Our society has gotten much better at servicing nearly all of our most basic drives:

- Hunger. Food today is more abundant, convenient, palatable and cheaper than ever before. Nearly all of our diet-related health problems come from eating too much, not from nutritional deficiencies or toxic food additives.

- Entertainment. Infinite feeds of short-form video, algorithmically tailored to our personal interests. Our dwindling ability to read books and think deeply is directly related to the always-on faucet of easy entertainment.

- Romance. Swipe right, swipe left. An infinite sea of potential mates at our fingertips, allowing us either to indulge forever in short-term hookups or scrutinize endlessly to find the perfect partner, who, of course, doesn’t actually exist.

- Physical ease. Our physical environment requires increasingly less effort. The result is that we don’t move enough and are sicker as a result.

It’s easy to blame “capitalism” or big corporations or some other nefarious force for all of this. After all, if the big tech companies didn’t insist on making phones so addictive, maybe we would read more books. And if industrial food producers didn’t make such ultra-processed junk, we wouldn’t have so many health problems.

But the companies are all locked into the same bind. If Meta doesn’t make the most addictive social media website, they’ll be outcompeted in the attentional marketplace by ByteDance or YouTube or some new start-up that will give people what they desire.

The real fault isn’t in the companies, but in ourselves.

Victims of Our Own Success

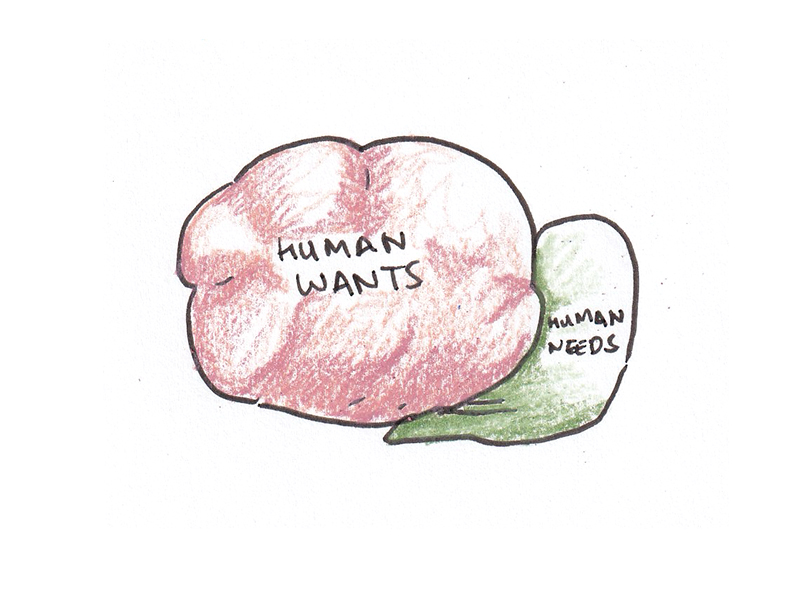

As we’ve become richer and more technologically advanced, we’ve become better at delivering the things people want—but what we want isn’t always what we need.

It’s hard to describe our current moment as a utopia with a straight face. Indeed, I have a lot of fears and misgivings about the direction society is taking. I’m worried about democracy, war, warming, divisiveness and the possibility that the robots will eventually kill us all.

But if we define a utopia as a society that gives people an abundance of the things they want, then, at least compared to nearly all actually-existing societies, we’re living in it! True, there are still problems that might be solved in some glorified Star Trek future that don’t exist today: teleportation, robot butlers, cures for aging, and world peace. But if we avoid speculative futures, it’s pretty clear that we’re closer to the utopia of human desires than we’ve ever been in the past.

Yet, if we look at human flourishing, the kinds of things we need to be psychologically fulfilled, the picture doesn’t look so good. Rates of depression and anxiety have skyrocketed. People are anxious, fearful, inattentive and unhappy.

One story you can tell about this trend is that technology is to blame. The rise of smartphones, social media and easy entertainment have glued us to screens rather than real friends, hobbies and time for reflection. If so, the problem would be not that we live in a world without those things (friends, hobbies and time for reflection still exist, after all), but that our world has too much the things people desire, and they crowd out the things we actually need.

Stoicism, Social Control and Ozempic

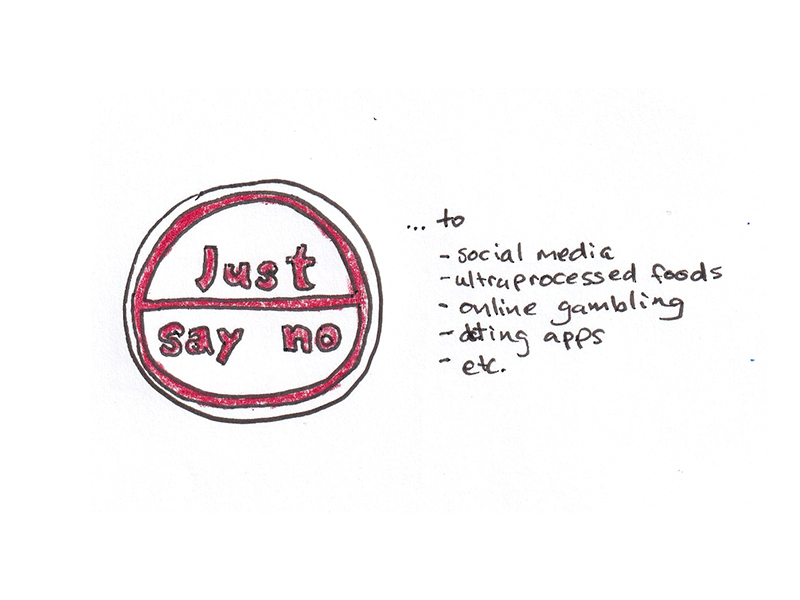

If this diagnosis is correct, what can we do about it? I see only three options, all of which have serious drawbacks.

The first is prudence. Cultivate virtue. Resist vice. Delete social media from your phone. Buy only veggies and whole grains for your pantry. Don’t drink, gamble or own a television.

I’m sympathetic to this path. And, given that this is the only factor that we can, as individuals, realistically change, it’s usually the one I spend more time advocating. It requires recognizing that there has always been a tug-of-war in the human soul between the steeds of passion and reason, but in today’s world the passions are being pulled by a rocket ship.

But, if “have more willpower” was a universal solution, we’d have adopted it by now. Losing weight by eating fewer calories than you burn has always worked. But sustaining weight loss through willpower alone has astonishingly low success rates.

I don’t think this failure of willpower means we should stop trying. But if we’re in an escalating arms race with technology increasingly able to satisfy our most basic drives, that effect isn’t going to be balanced with increasing willpower by all but the saintly few.

The second option is regulation. Tax sodas. Ban smartphones from school. Force social media platforms to moderate content and change their algorithms.

This path has the advantage of not relying on the limits of human willpower. If ultra-processed foods become illegal, we won’t need to use self-discipline to avoid eating them.

But I’m also skeptical that social control can ever provide the full solution in a democratic society.

In Julia Belluz and Kevin Hall’s book Food Intelligence, the authors go to great lengths to describe how the hyperpalatable and over-processed food environment is making us fat and sick. But, when they get to the section of what to do about this, it becomes clear that the solutions that would actually work would be draconian.

Banning soda, junk food, fast food and anything ultra-processed would work, but outside of a few health-obsessed foodies, I doubt it could reach a critical mass of acceptance in society. If prohibition didn’t work for alcohol, it’s hard to imagine a scenario where it would work for donuts.

The kinds of social control we’re more likely to get are those where only a minority is impacted. Smartphone bans in school are popular because kids don’t get a vote. Smartphone bans for grown ups, in contrast, feel like a violation of civil rights.

Similarly, my country, Canada, is considering banning smoking permanently for those born after a certain year. I understand the impulse. But it’s only popular because most people don’t smoke at all. Alcohol also causes many social harms, but I see no similar proposals for banning booze, because teetotalers are in the minority.

Ultimately, I have a hard time understanding the people who scoff at the idea of individuals applying willpower and habit changes to avoid vice, yet seem enthusiastic about solving the problem with government regulation and control. The same people who don’t have enough willpower to avoid overeating and obsessive phone usage are, supposedly, the same people who will vote for a policy to prevent them from accessing the objects of their desires.2

So, if willpower is weak and social regulation requires collective willpower, what does that leave us with?

The third option seems to be: use technology to modify our brains to change what we actually want.

Until recently, this would have been the premise of a (probably dystopian) science fiction novel. But with the arrival of GLP-1 agonists, it’s the world we’re now living in. GLP-1 drugs work not by speeding up your metabolism or preventing you from accumulating fat but by changing how much you want to eat in the first place. Users experience reduced “food noise” and cravings for junk food. Grocery stores are apparently even going to need to increase the amount of produce they stock, as a new group of shoppers suddenly feel the urge to buy kale and broccoli.

The effects don’t seem to be entirely limited to eating behaviors either, with some early reports suggesting the medications may help with other kinds of addictive behaviors such as drug abuse or alcoholism.

GLP-1 drugs seem to work well with few major side-effects, but they’re hardly the only example. ADHD cases have exploded, in part due to loosening diagnostic criteria. But also because inattentiveness is a spectrum and paying attention is harder than it used to be. Medications may make it easier for people to focus and ignore distractions. Unfortunately, the side-effects of these drugs are probably worse than GLP-1s, but it’s possible to imagine a new focus wonder drug of the future that has fewer side-effects and more widespread adoption.

I find it hard to get enthused about a future where we create an abundance of human vices, and cure that abundance by creating drugs that make us desire them less. It sounds, well, dystopian. But I suspect that this will end up being the path humanity follows, if only because it is easiest.

I'm a Wall Street Journal bestselling author, podcast host, computer programmer and an avid reader. Since 2006, I've published weekly essays on this website to help people like you learn and think better. My work has been featured in The New York Times, BBC, TEDx, Pocket, Business Insider and more. I don't promise I have all the answers, just a place to start.

I'm a Wall Street Journal bestselling author, podcast host, computer programmer and an avid reader. Since 2006, I've published weekly essays on this website to help people like you learn and think better. My work has been featured in The New York Times, BBC, TEDx, Pocket, Business Insider and more. I don't promise I have all the answers, just a place to start.